CVS: The One-Stop Shop for Pharmacy Needs

Analyst: Young Money Capital

CVS Business Background

CVS Pharmacy competes in three different segments: health care benefits segment, pharmacy services segment, and retail/LTC. The health care benefits segment includes Aetna, an insurance company that was acquired by CVS in 2018 for $69bn. The pharmacy services segment includes where customers get prescriptions filled. The retail/LTC segment includes front-of-the-store merchandise and the MinuteClinic/Health Hub.

CVS Segment Breakdown

Source Author Data from CVS Investor Relations

CVS stock chart bottomed shortly after the acquisition of Aetna, as many people believed they overpaid and would face competition from Telehealth. CVS has instead turned into a one-stop shop for all your health care needs. Customers can walk into their Minute Clinic and get seen by a doctor, prescribed medicine at the pharmacy, and pay for it with their Aetna insurance all in the same location.

CVS Stock Price

Source: Yahoo Finance

Industry Overview

In the pharmacy industry, CVS is the largest player and makes up about 25% of the total market share of prescriptions according to Statista, and 27% according to themselves. They have increased their share by about .6% from Q4 2020. The next largest competitor is Walgreens which has about 19% market share in the pharmacy industry according to Statista.

Independent Pharmacies are still a major factor in the industry making up about 1/3 of all pharmacy locations. Their market share and store count have been decreasing over the last five years. CVS has kept its store count essentially flat but has increased its market share by increasing efficiency.

CVS is the Industry Leader in Prescriptions

Source: CVS Earnings Presentation

Competitive Advantage

CVS’s scale, vertical/horizontal integration provides them with a moat. Companies in the telehealth industry are trying to disrupt CVS by offering telephone screenings and mailing prescriptions. These companies take a capital-light approach which could easily be replicated. CVS takes an omnichannel as they offer in-store and online screenings and prescriptions. CVS can do what the disruptors are doing and provide more value with their brick-and-mortar locations and cost advantages.

CVS’s incredible scale allows for superior customer convenience and cost advantages. They have a pharmacy within ten miles of 85% of the US population. This gives the customer the option of going into CVS to quickly obtain their prescription, or wait for a delivery. Most customers are time-sensitive and want their prescriptions immediately. Telehealth companies cannot replicate this build-out as it is too capital intensive.

Source: ScrapeHero

CVS’s advantage in scale also shows up in its drug prices. Since CVS has a ~27% market share, they can better negotiate prices and obtain volume-based discounts with drug producers as drug producers need to offer their drugs at CVS locations. This lowers CVS’s costs and allows CVS to pass the savings onto their customers. All other competitors are smaller than CVS, thus, cannot pass on the same cost advantages CVS can. CVS also processes ~2bn of the ~6bn prescriptions in the United States. There are fixed cost advantages from processing prescriptions that CVS benefits from as well.

CVS’s MinuteClinic and health hub provides a moat and is a strong driver of same-store sales. These services allow customers to get screened and prescribed a prescription in-store, providing unparalleled convenience for their customers. These services do not take up much room in the store driving same-store sales and sales per sq. foot. Currently, CVS has 45% coverage of the US population by the MinuteClinic and Health Hub. CVS’s management has continued to focus on expanding its MinuteClinic offering which has a sizeable runway remaining.

CVS’s acquisition of Aetna provides vertical integration and cost advantages for both the pharmacy and MinuteClinic/Health Hub services. Aetna is the third-largest insurer that Morningstar covers and Aetna has 24 million customers. The leaders, UnitedHealth and Anthem, each serve around 45 million customers. The prescriptions and MinuteClinic/Health Hub offer insurable services and Aetna is an option for both of these products. CVS can create cost savings for customers who use all CVS products and do not venture outside of their eco-system.

CVS’s one-stop-shop eco-system can be visualized by the graphic below. Customers are drawn to CVS by either their pharmacy or MinuteClinic. The pharmacy and MinuteClinic are horizontally integrated and both increase the value of each other because of their convenience for customers. Aetna supports both of these segments and provides vertical integration and cost advantages.

CVS's Vertical and Horizontal Integration

Source: Author

Optionality

CVS has an opportunity for growth in mailing prescriptions to customers. There is a lot of attention on high-flying health care companies that mail prescriptions and for good reason. Future Market Insights projects the prescription delivery services industry to grow at a CAGR of 18% until 2030. Currently, CVS only has ~15% of their prescriptions mailed, but it equals around 40% of their pharmacy services revenue. Mailing prescriptions will increase sales per sq. foot and ROIC because less capital is required for brick-and-mortar stores. This could allow CVS to expand margins and accelerate pharmacy services revenue growth. The threat of this is it could cannibalize their Retail/LTC business as many people buy CVS goods while picking up a prescription.

Management/Use of Cash

Karen Lynch took over as CEO of CVS in February of 2021. She formerly worked for Aetna which was acquired by CVS in 2018. Karen Lynch initially used CVS’s cash to pay down the debt from the Aetna acquisition. Now that CVS is approaching its optimal debt level, Karen Lynch has reinvested into MinuteClinic, increased the dividend, and authorized a large share buyback. The MinuteClinic is a smart investment because of its high ROIC and it increases the value of CVS’s other services. The quarterly dividend has increased from $0.50 per share to $0.55 per share which is a 10% increase. $10bn remaining from share repurchase from Dec 9th share repurchase program or ~7.5% of the float. CVS has a strong cash flow business which allows for ample reinvestment and returning value to shareholders

Risks

CVS’s main risk comes in the form of regulation. Increasingly, politicians have been focused on creating a system for affordable health care for Americans, and regulations to this industry could adversely affect CVS. For the immediate future, this risk looks unlikely to happen, but it could become a terminal value risk.

Valuation

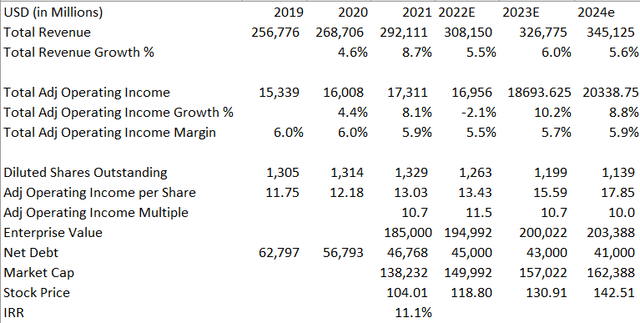

While I try to give my readers actionable ideas, I believe the market has correctly valued CVS. I expect revenue for 2022 to be at the higher end of their guided range. I expect CVS to be able to grow its revenue between 5-6% over the next few years and for the operating margin to range between 5.5-6%. I expect CVS to have an IRR of 11.1% at the current price levels as shown by the valuation grid below. I do believe CVS has a strong moat and could be a buying opportunity on a significant price drop.

Total Company Valuation

Source: Author, Historical Data from CVS Investor Relations

My segment analysis so readers can better understand the assumptions is shown below.

Health Care Benefits

Source: Author, Historical Data from CVS Investor Relations

Pharmacy Services

Source: Author, Historical Data from CVS Investor Relations

Retail/LTC

Source: Author, Historical Data from CVS Investor Relations

Other

Source: Author, Historical Data from CVS Investor Relations

Disclosure: I have no current position in CVS stock