FICO: The Industry Standard

FICO: The Industry Standard

Analyst: Young Money Capital

Business Overview

Fico was founded in 1956 by William Fair and Earl Isaac hence the name Fair Isaac Corporation. Today, Fico is a twelve-billion-dollar company that is deeply embedded in the credit rating industry. They operate in two segments: scores, which includes their famous Fico scores, and software, which leverages their Fico scores. Both segments account for roughly half of their revenue, but their scores segment accounts for about 84% of their operating income.

Industry Overview

Fico scores are synonymous with lending. Fico licenses their scores to lenders for mortgage, auto, and home loans. Fico scores started as a way to accurately predict a borrower’s ability to repay the loan. Since then, many lenders have built their own proprietary lending algorithms, but Fico scores still have a lot of value as they’re a standard. Fico scores have become a way for lenders to communicate with other organizations and borrowers without having to reference their unknown proprietary method.

Source: FICO Company Website

Fico estimates that it is used by 90% of the top lenders. Their most relevant competitor is Vantage Score, but Vantage Score has a much smaller market share and nowhere near the name recognition. Fico has sold over 10 billion scores in the last 12 months.

Competitive Advantage

Scores

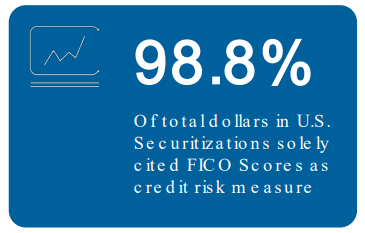

Fico has become the standard for selling loans between banks. Banks are not familiar with another bank’s underwriting system so they have to use Fico scores. 98.8% of dollars securitized in the US solely cite Fico scores as a risk measurement emphasizing its importance.

They have such a large market share because “FICO scores are a standard because everyone's using it and securitizing everything with them. It's also a currency that people use. FICO sits at the center of the lending ecosystem and provides tremendous utility. It has increasing returns and network effects that come from having a lot of nodes on the network.” - Eagle Point Capital

The Wall Street Journal further explained it as:

FICO has a big advantage: Investors rely heavily on the scores to decide whether to buy packaged-up consumer loans. The scores are a common language of sorts, one that requires no time-consuming translation. Even lenders that don’t use FICO to make lending decisions tend to use them in loan securitizations. - Wall Street Journal

Source: FICO Investor Relations

Constantly, lenders are under more scrutiny for who they give and don’t give loans to. Fico scores are quantitative scores that are understood by borrowers. Lenders are able to tell a declined customer your Fico score was too low and you need to raise it which saves a lot of time and aggravation. These scores are already well understood by customers as they have a 90% brand awareness in the US. Customers are not familiar with Vantage Scores or internal proprietary scores which will cause a lot of confusion.

Fico scores have an added advantage for mortgage loans. It is the law that lenders have to use Fico scores.

In Fico’s most recent 10k they stated A significant portion of our revenues in our Scores segment is attributable to the U.S. mortgage market, which includes, for conforming mortgages in that market, a requirement of The Federal National Mortgage Association (“Fannie Mae”) and The Federal Home Loan Mortgage Corporation (“Freddie Mac”) that U.S. lenders provide FICO® Scores for each mortgage delivered to them. - FICO SEC Filing

While Vantage Score is trying to reverse this legislation, it provides a significant barrier to entry for anyone trying to enter the mortgage scoring business.

Fico scores add a ton of value and they’re incredibly cheap. The average cost last year was about 6.5 cents although the score cost varies considerably depending on the customer and what the score is used for. (author calculation from 10 bn scores sold divided by 654 million in scores revenue). This is an extremely small price to pay for a lender deciding to give a customer a $500,000 home loan or a $20,000 car loan.

From 1991 to 2016, Fico did not raise the prices of their scores. In 2016 and 2017 they increased them in line with inflation and did not receive any pushback from customers. In 2018, Fico management renegotiated their contracts to allow special pricing increases.

They do not release how much their special pricing increases were, but it would be reasonable to estimate their average special pricing increase would be over 10% each year. It is important to note, that management stated they do not raise prices evenly as some segments have more pricing power than others. This price increase has shown up on their revenue line. Fico’s scores revenue has increased at a CAGR of 26% since 2018. Management stated for this year “There's been no change in our strategy or approach to special pricing.”

Software

Fico also has a software side to their business that focuses on credit decision making, portfolio management, fraud, and more. The software that Fico offers has Fico scores ingrained into their software making this a logical vertical integration. 95/100 of the largest US financial institutions are Fico clients and use Fico scores through their platform. A large customer base shows how Fico scores and their software are the standards for securitization. There are high switching costs in changing software systems, especially ones that are so integral to a company’s success like loan securitization. There are also network effects protecting Fico. Banks use FICO's software to communicate and trade with other banks. Their scores are the standard and their software being the default choice further insulates it.

Fico also has a fraud prevention side to the business. Fico protects over 2 billion accounts and 90+ billion dollars per year are saved by Fico’s anti-fraud offering. Fico’s scale should not be surprising as it is the industry leader in enterprise fraud solutions according to Chartis.

Enterprise Fraud Solutions Quadrant

Source: Chartis

Fico’s software segment revenue has declined from 739 million to 662 million from 2019 to 2021. This is explained by their transition to annual recurring revenue (ARR), focus on platform solutions, and a key divesture impacting the top line. The platform revenue is starting to become big enough to have an impact on the revenue line.

Fico’s management team talked about the success of the transition by stating “With the caveat that this is not guidance, I would say look at our platform growth, 50% platform growth, which tells you that we have something there that the market wants. We have a large number -- a large number -- 19 enterprise customers, large customers who have adopted the platform and many more in the pipeline.” - FICO Earnings Call

The success of this transition and strength of Fico’s moat is shown by Fico’s platform dollar-based net expansion rate (DNRR) accelerating from 112% in March 2020 to 143% last quarter.

Fico’s Dollar Based Net Expansion Rate

Source: FICO Investor Relations

Management Team/Use of Cash

Fico’s management team's focus has been on reducing Fico’s share count. In 2010, Fico had 45,308,000 diluted shares outstanding, and last quarter they had 27,524,000.

Fico’s management strategy has been to lever up and buy back more shares.

In fiscal 2021, … we increased our leverage by about $425 million compared to year-end fiscal '20, but our adjusted leverage ratio remains a modest 2.07 times. We view FICO shares as the best use of our excess cash at this time and expect to continue to aggressively buy back shares in the coming year. - FICO Earnings Call

This commitment to buying back shares is not stopping.

I’m pleased to say we repurchased more than 1.2 million shares in our first quarter and more shares in January. Our buybacks reduced the outstanding shares by 9% versus Q1 of last year and this morning, we announced the new $500 million Board repurchase authorization. - FICO Earnings Call

When they have this incredible of a business, who can blame them?

Risks

Bears claim that Fico scores do not have as strong of predictive power as vantage scores, Upstart, or Affirm and believe Fico is ripe for disruption. This claim is irrelevant to understanding Fico’s competitive advantage. Fico’s is the industry standard, the common language, and is ingrained into financial institutions and their predictive power is largely irrelevant to the moat of the company.

Valuation

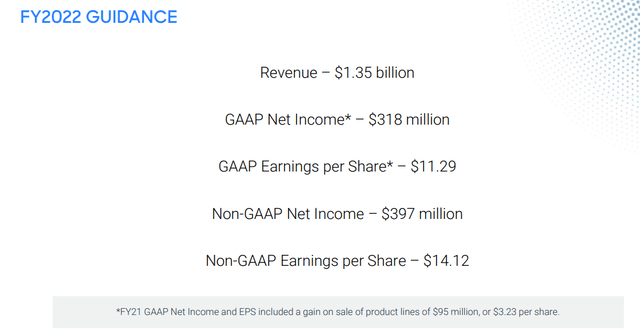

Fico management takes understating guidance to an extreme.

Management stated “we expect the Scores business to grow about 6%. There's been no change in our strategy or approach to special pricing. Accordingly, special pricing increases consistent with the past several years are not included in this guidance. While we expect these price increases to have an impact consistent with those over the last several years, because it's difficult to estimate the timing and the magnitude of the impact, we remain conservative in how we issue our guidance relative to such increases.” - FICO Earnings Call

The vast majority of Fico’s revenue growth comes from its special pricing increases. On top of that, Fico does not include the shares they repurchased as part of their guidance, even though they already repurchased many shares. They are setting themselves up for another easy beat on the top and bottom line.

FICO Guidance

Source: FICO Investor Relations

Fico’s scores revenue should come in very similar to prior years. A modest decline in top-line revenue growth should be expected. They have a very strong moat which protects them from the competition, but there will eventually be limits to how much they raise prices.

Scores Segment

Source: Author Historical Data from SEC Filings

On the software side of the business, I project the platform side of the business to continue to be the growth driver. I also expect margins to modestly expand as they continue to transition to an ARR model.

Software Segment

Source: Author Historical Data from SEC Filings

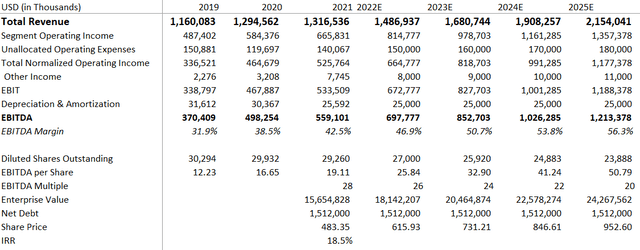

The scores revenue increase is almost all incremental profit. On the software side, margins expanding will help EBITDA margins expand. Factoring in some multiple compression, and using the below assumptions, Fico should have an IRR of 18.5% providing a good buying opportunity for long-term investors.

Company-Wide Projections

Source: Author Historical Data from SEC Filings

Disclosure: I/we have a beneficial long position in the shares of FICO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.