Finvolution Investment Report

Finvolution Investment Report

Analyst: Young Money Capital

Investment thesis

Finvolution has a dominant market position in the Chinese micro-lending industry. They issue loans with an average interest rate of 24.3% and have a 90+ day delinquency rate of 1.04% resulting in an extremely efficient 14.8% ROA after my adjustments (shown in valuation section).[1] The company has geographic optionality with their recent expansion into Indonesia and product optionality by starting to offer loans to small business owners. The stock trades at a reasonable 1.12 P/B which effectively values them at their current portfolio of loans and ignores their market positioning and future loan making capabilities. Finvolution’s four co-founders are still involved with the company and their Chief Innovation Officer and co-founder Shaofeng Gu owns 29.6% of the company which he added to in 2020, further aligning investors incentives with Finvolution.[2]

Industry Overview and Regulation

Micro borrowing initially started as a non-profit business for developing nations to increase economic activity. Charities would give short term, small loans to individuals and eventually would be repaid. Charities found that the repayment rate was similar to developed markets retail banking repayment rates, but they were not able to scale because of operational inefficiencies and not receiving interest on their loans.

Multiple for-profit corporations, including Finvolution, created peer-to-peer lending platforms to fix the scaling problem. They facilitated the matching of borrowers and lenders. In mid 2018-mid 2019, China changed regulations and forced companies to loan themselves, transforming micro-borrower’s business models. Finvolution adjusted to this regulation and grew their loan transaction volume, while their competitors are still struggling to adapt.

China is now capping loan interest rates at 24%.[3] Prior to the announcement, Finvolution has started targeted higher quality borrowers while Qudian, Finvolution’s biggest competitor, targeted the higher risk higher interest segment. Finvolution stated that 80% of their loans are at an interest rate of 24% or lower last quarter and will continue to trend that way with minimal impact from the regulation.[4] Qudian did not release the same metrics, but they stated on their most recent earnings call “local regulators have very different implementation details and time lines on this issue, given the fact that our profitability will be negatively affected if our interest rates gets capped at 24%. So before any concrete interest rate restrictions get enforced on our proprietary lending activities, we will choose to maintain our status quo, that is we charge at less than 36%.”[5] Finvolution will come out of the additional regulation stronger and be able to take even more market share from their smaller, less efficient competitors. Qudian will be forced to transform their business strategy, again.

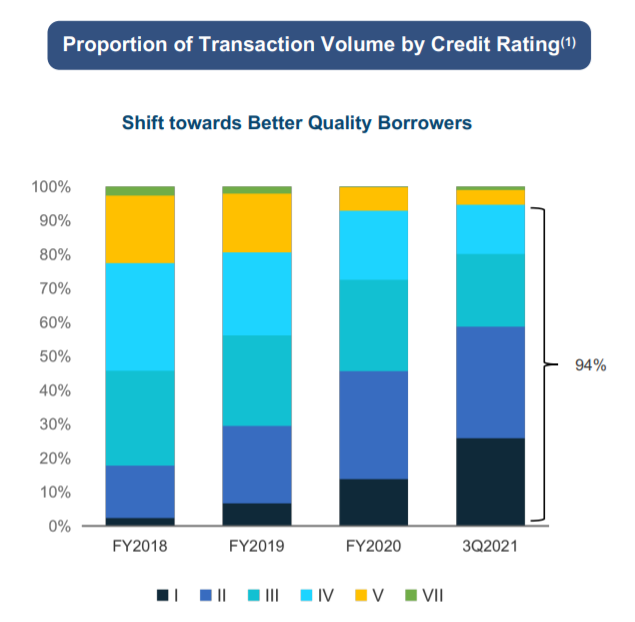

Finvolution Borrower Quality Improvement

Finvolution 2021 Q3 Earnings Presentation https://ir.finvgroup.com/Financial-Results

Competitive Advantage/ KPIs

Finvolution’s competitive advantage rests on their proprietary credit assessment model, their 60+ hard to replicate relationships with financial institutions, and their economies of scale.

Finvolution developed their “magic mirror” credit risk assessment model that detects fraud and anomalies, scores credit risk, and gives due date reminders to borrowers. It is a machine learning based model that improves, like any machine learning model, with more data. Finvolution is more than ten times larger than Qudian by loan volume allowing their model to have more data than the competitors, thus, a better model. Finvolution’s model has continuously improved their delinquency rate, along with better macro environment conditions, and the shift to higher quality borrowers.

Finvolution’s Improving Delinquency Rates

Finvolution 2021 Q3 Earnings Presentation https://ir.finvgroup.com/Financial-Results

Finvolution also has relationships with around 60 licensed financial institutions in China and Indonesia to help secure funding or new customers. This allows Finvolution to scale and these relationships are difficult to replicate. Finvolution’s track record and executive management team have allowed them to secure these relationships. Currently, is trying to build more relationships to scale. In the long term, Finvolution should be able to negotiate better funding terms with these institutions because Finvolution’s funding sources are fragmented and the micro-lending industry is consolidated.

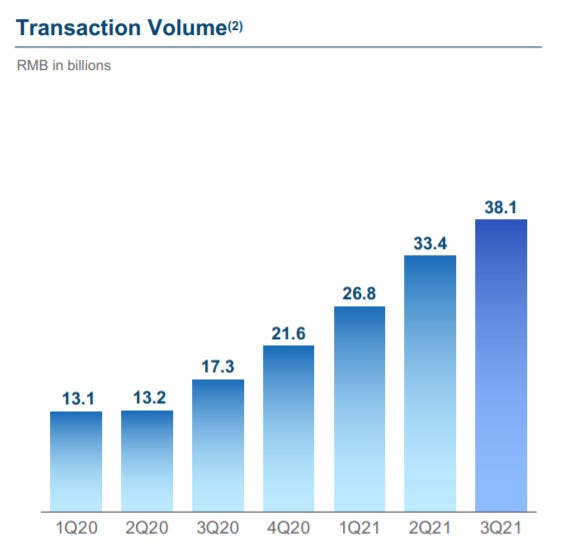

The key KPIs for Finvolution are their ROA and transaction volume. Since Finvolution’s book value is their loan portfolio, their ROA should be calculated as growth in book value divided by assets (to eliminate the effect of leverage and measure efficiency). Finvolution’s trailing twelve month ROA is an extremely efficient 14.8% (see valuation table for full calculations and projections). With a ROA of 14.8% Finvolution’s largest limitation is the amount of loans they can make. Finvolution’s transaction volume should be tracked to ensure that they have a strong pipeline of future loans. In their most recent earnings call Finvolution raised guidance and “expects a year-over-year increase of 103% to 111% in transaction volume”.[6] This enormous growth in transaction volume will allow Finvolution to continue to scale.

Finvolution Transaction Volume by Quarter

Finvolution 2021 Q3 Earnings Presentation https://ir.finvgroup.com/Financial-Results

Optionality

Finvolution’s biggest need is to acquire more customers. They have recently expanded into the small business market as opposed to individuals and expanded internationally. Small business owners accounted for 21% of their total transaction volume. The total number of small business owner customers grew 20% from the prior quarter. Finvolution also stated that the small business segment has a “more supportive regulatory environment” then the individual borrower’s segment. [7]

Finvolution has also recently entered foreign markets Indonesia, Philippines, and Vietnam. “The countries which we have already established a presence have massive market opportunities. For example, Indonesia, Philippines and Vietnam have a combined population of around 500 million. It is higher than the U.S. population and it is not small compared to China. And its loan to GDP ratio is about 8.3% with a low-credit penetration rate of between 3% to 4%.”[8] Recently, they partnered with PT Bank Jago to help facilitate loans and JD Indonesia to enter into the buy now pay later sector. Finvolution will continue to invest in these initiatives driving loan transaction volume growth.[9]

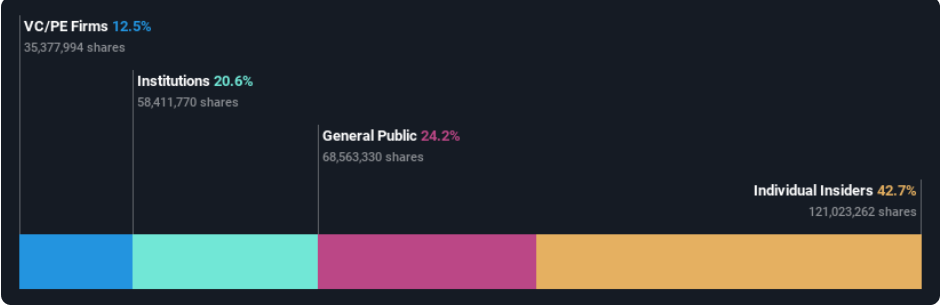

Insider Ownership/Capital Allocation

Finvolution Ownership Summary

Simply Wall St https://www.yahoo.com/now/institutions-own-finvolution-group-nyse-103216102.html

Finvolution has 42.7% insider ownership. In the fourth quarter of 2020, Co-founder, Chief Innovation Officer, and Board of Director Chairman, Shaofeng Gu purchased 530,000 shares of Finvolution. He now owns 29.6% of shares outstanding.[10] Co-founder and Board of Director, Jun Zhang, owns 7.2% of the shares outstanding.[11] All four co-founders are still involved with the company. The strong insider ownership aligns shareholder interests with managements.

Finvolution allocates their capital by share repurchases, dividends, and reinvesting in new expansion opportunities. On August 25th of 2020, Finvolution announced that they have repurchased $111 million usd of Finvolution shares since 2018 and expanded their share repurchase program to buy back a cumulative $180 million usd of Finvolution shares by the end of 2021.[12] Finvolution has also offered a 2.74% dividend yield (as of November 24, 2021). Finvolution’s management is doing an excellent job returning capital to shareholders. They have also reinvested money into their core business and expansion efforts that were previously mentioned in the optionality paragraph.

Key Risk

Finvolution’s key risk is Chinese regulation. All Chinese companies are risky and the micro-lending industry is one of the riskiest industries. Lending money in China is often considered taboo and regulators have cracked down on the industry in the past. Finvolution has fully cooperated with regulators, and has been proactive. While there are significant risks to the industry, Finvolution’s attractive positioning and valuation an attractive investment for those willing to stomach the risk and volatility.

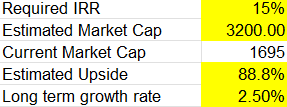

Valuation

Normally, Valuations should be based on earnings, however, for financial and insurance companies, growth in book value should be used because it is often a leading indicator because that is the marketable value of the loan portfolio. ROA Annual is an return on asset calculation for the trailing twelve months from that period. ROA Quarterly Annualized is an return on asset calculation for that quarter extrapolated for a full year performance. Three quarters for Finvolution have been reported so far in 2021 with the last one still outstanding. A relatively high required IRR of 15% was used to account for the high risk nature of the investment. The estimated market cap was calculate by 2022 growth in book value divided by (Required IRR - Long term growth rate). The long term growth rate value is conservative given the growing nature of the industry.

Disclosure: I/we have a beneficial long position in the shares of FINV either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

[1] Finvolution 2021 Q3 Earnings Release https://ir.finvgroup.com/Financial-Results

[2] Finvolution SEC Filing https://ir.finvgroup.com/2021-01-11-FinVolution-Group-Announces-Continued-Purchase-of-Shares-by-Chairman

[3] Qudian 2021 Q2 Earnings Call https://ir.qudian.com/static-files/55661466-1a43-4bdf-a295-a0fe1c744f09

[4] Finvolution 2021 Q3 Earnings Release https://ir.finvgroup.com/Financial-Results

[5] Qudian 2021 Q2 Earnings Call https://ir.qudian.com/static-files/55661466-1a43-4bdf-a295-a0fe1c744f09

[6] Finvolution 2021 Q3 Earnings Call https://ir.finvgroup.com/Financial-Results

[7] Finvolution 2021 Q3 Earnings Call https://ir.finvgroup.com/Financial-Results

[8] Finvolution 2021 Q3 Earnings Call https://ir.finvgroup.com/Financial-Results

[9] Finvolution 2021 Q3 Earnings Call https://ir.finvgroup.com/Financial-Results

[10] Finvolution SEC Filing https://ir.finvgroup.com/2021-01-11-FinVolution-Group-Announces-Continued-Purchase-of-Shares-by-Chairman

[11] Simply Wall St https://www.yahoo.com/now/institutions-own-finvolution-group-nyse-103216102.html.

[12] Finvolution SEC Filing https://ir.finvgroup.com/2021-01-11-FinVolution-Group-Announces-Continued-Purchase-of-Shares-by-Chairman