Guest Article: Tesla’s Direct-To-Consumer Advantage

Written by: @fteric https://twitter.com/ftreric

This week Eric Sprague is doing a guest article for Young Money Capital’s Newsletter. He did a deep dive into Tesla’s direct-to-consumer advantage. It is very informative and a competitive advantage that is not often talked about. His Twitter handle is @fteric and his seeking alpha profile is https://seekingalpha.com/author/eric-sprague#regular_articles.

-Tesla’s direct-to-consumer approach allows them to control the retail experience in a manner similar to what we see with Apple stores

-90% of Model S service issues can be identified remotely and 80% of fixes can be done at the home or office of the car’s owner.

-Electric vehicles require little in the way of service but wholesale dealers make much of their gross profit on service.

Introduction

My thesis is that Tesla (TSLA) is advantaged because of their longstanding direct-to-consumer model. Legacy carmakers mainly use the wholesale model where they sell vehicles to dealers and dealers then sell vehicles to customers.

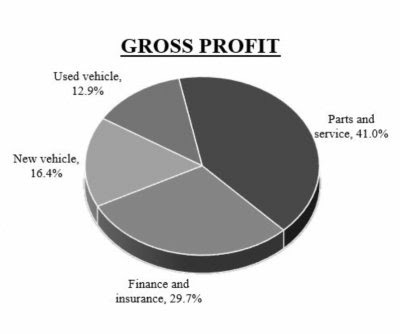

Electric cars sold direct-to-consumer online are the future but legacy automakers are held back by their wholesale dealers. Electric vehicles [EVs] have fewer moving parts than internal combustion engine [ICE] vehicles and they need less on-premise maintenance than ICEs - almost none by comparison. Incentives matter significantly and dealers are not incentivized to sell EVs over ICEs because much of their gross profit comes from service and maintenance. A graphic from the AutoNation (AN) 2020 10-K shows that 41% of their gross profit comes from parts and service:

Image Source: AutoNation 2020 10-K

The electrification dilemma placed on wholesale dealers is confirmed per the McKinsey Automotive September 2020 Report: A future beyond brick and mortar - disruptive change ahead in automotive retail:

After-sales revenues and profits will come under big pressure, as EVs have fewer moving parts and need less maintenance. For example, oil changes are currently a huge profit driver that will ultimately dissolve for dealerships.

Tesla Before 2010

Power Play by Tim Higgins explains how Tesla cemented their advantage with their direct-to-consumer sales model many years ago when they were figuring out how to sell the Roadster. Tesla CEO Elon Musk has always wanted to change the way cars are sold. His thought process is revealed around the time of Tesla’s original business plan before 2007; he wanted to be able to take control of the car buying experience.

Tesla co-founder Martin Eberhard’s original plan for Tesla depended upon using exotic franchise dealerships in upscale neighborhoods to sell the Roadster but that path was altered. Bill Smythe owned a successful Mercedes dealership and Eberhard relied on him for advice. Telling Eberhard that he didn’t trust any of the dealers, Smythe caused Eberhard to recommend a direct-to-consumer approach to Tesla’s CEO Musk wanted more than just a direct-to-consumer buying experience; he wanted an online buying experience. Per Power Play, this is why he put eBay’s automotive marketplace creator, Simon Rothman, on Tesla’s board. CEO Musk wanted to keep sales online-only but board members debated with him. Eberhard and others worried that customers needed hand holding to understand new technology. And of course anyone who has taken a Tesla for a test drive knows that this is an impactful occurrence.

Selling direct in California was an option for Tesla because of a technicality per Power Play:

Their lawyer advised them that Tesla could sell directly in California on a technicality: the carmaker had never had any franchise dealerships, and therefore it wouldn’t be cutting into its franchisee sales. That, at least, was the argument they’d be building off of. Now they just needed to figure out the rules for forty-nine other states.

[Kindle Location: 843]

McKinsey Automotive Retail Report Findings

Insisting on direct-to-consumer sales from the beginning, CEO Musk was prescient and legacy automakers still haven’t caught on to the way cars will be sold in the future apart from small initiatives. Automotive retailing is transforming pretty slowly per the September 2020 McKinsey report. It surveyed more than 3,000 car buyers in China, Germany and the US. Daimler has shifted to a direct sales model with pilots in Sweden and South Africa in 2019. Daimler is also experimenting with a direct strategy in Austria and parts of Australia for the EQC and other EQ electric models to be launched by late 2023. Toyota launched their direct Drive Happy Project in New Zealand where new vehicle stock is stored in 3 pools owned by Toyota.

The report focuses on what they call ACES trends - autonomous driving, connectivity, electrification, and shared mobility. Digitization is also stressed in the report and it is noted that more than 80% of customers already use online sources during the car-buying process. Brick and mortar locations are needed for test drives but they don’t have to be franchise dealers.

The McKinsey report talks about factors for the slow speed of change to digitization and they refer to automakers as OEMs [Original Equipment Manufacturers]:

Among these are existing dealer franchise laws, infrastructure development, dealer involvement, and challenges in developing a compelling digital car experience and test-drive alternatives. Changing this model will take time and requires close collaboration between OEMs, dealers, and selected new partners across the retail chain, but our research shows that digital is becoming more important.

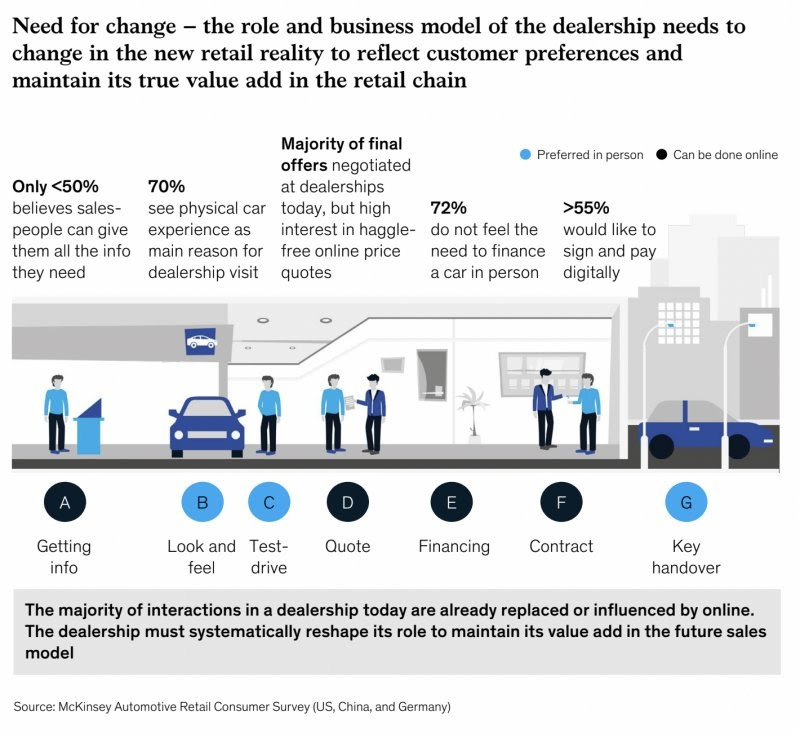

Visual inspections, test-drives and handovers are the only parts of the car buying experience that are preferred in person per the McKinsey report:

Image Source: McKinsey Automotive September 2020 Report: A future beyond brick and mortar - disruptive change ahead in automotive retail

This part of the report is extremely alarming because customers rely on biased salespeople for information about EVs:

When thinking about future car purchases, our research showed that 41% of customers expect dealers to be a superior source of knowledge and product expertise, especially in the areas of connected services, driver-assistance features and electrification. They also want to be able to access on-site information related to internal combustion engine [ICE] alternatives [e.g., battery EVs and hybrid EVs] and other vehicle technology. This can be achieved either through talking to experts [e.g., product geniuses] or via information terminals that allow customers to access detailed information independently, at their own speed, and in a non sales environment.

Customers want to rely on franchise salespeople at dealerships for information on EVs yet we know that EVs require little in the way of service where wholesale dealers make much of their gross profit!

Control The Retail Experience: Apple Stores

Power Play shares that Tesla had a little more than 10 stores by 2010 with plans to open 50 more. At this point Tesla was only making about 50 Roadsters a month. CEO Musk had noticed the success Apple (AAPL) was having with the expansion of their Apple stores and he wanted to find the person responsible. His name was George Blankenship and he’d opened 250 Gap stores before getting a call from Steve Jobs and helping Apple open more than 150 of their iconic stores. Blankenship thought about the way the knowledgeable staff and Genius Bar helped nudge customers into the digital age and how this template could be used for electric cars. Knowing that Tesla was sitting on an amazing product, Blankenship signed on and told Musk to use Apple’s retail approach. Like Apple, Tesla had loyal customers who were “evangelists” for the brand. Power Play tells of Blankenship’s Apple-like success in San Jose and the Denver-area:

We are revolutionizing the auto purchase and ownership experience,” Blankenship told the San Jose Mercury News. “At a typical car dealership, the goal of the dealer is to sell you a car that’s on the lot. At Tesla, we’re selling you a car that you design. The shift is people say: ‘I want this car.’ ” He quickly followed San Jose with a similar store just south of Denver, in the high-end Park Meadows mall. Foot traffic didn’t disappoint. The San Jose store received about 5,000 to 6,000 visitors per week after the initial burst of interest, double what Blankenship’s team had expected. The Denver-area store was getting 10,000 to 12,000 visitors per week.

[Kindle Location: 2,431]

Texas

It’s a crazy world we live in. Vehicles that Tesla makes in Texas have to be shipped out of state before folks in Texas can buy them! That’s not a typo, it’s a function of the byzantine franchise laws in Texas. Power Play gives us some background. Blankenship wanted to continue mimicking Apple stores in Texas after the Denver-area store but Texas was one of a small number of states that did not allow carmakers to sell directly to customers. Blankenship and a Tesla lawyer found that educational showrooms were allowed in Texas but not dealerships. Blankenship set up a gallery in Texas with educational material but no pricing. Customers who wanted to buy cars had to initiate contact on a computer and a Colorado call center would follow up with them.

Jumping ahead to 2013, Texas Automobile Dealers Association President Bill Wolters wanted to meet with CEO Musk and convince him that franchise dealerships could help with Model S sales. This was after Tesla had set up a gallery in Houston in 2011 and a second one in Austin. Of course the franchise profits were heavily skewed towards service and maintenance:

The typical franchise car dealer generated money on a mixture of new and used car sales, as well as servicing those vehicles. Overall, the average dealer that year made about $1.2 million in profit before taxes, selling 750 new vehicles and 588 used ones, according to the National Automobile Dealers Association. The service end of the business remained where the profit was. [On average that year, a new vehicle netted the dealer just $51.]

[Kindle Location: 3,224]

CEO Musk saw Wolters as an entitled incumbent from legacy systems who took customers for granted. CEO Musk told Wolters that Tesla would spend $1 billion to overturn ridiculous dealer franchise laws in America but they still have a ways to go in Texas.

Innovation

Per Power Play, General Motors (GM) CEO Dan Akerson drove a Tesla Model S around Detroit in the middle of 2013 to see what they were up against. He questioned R&D incentives at GM where they ranked as one of the largest holders of new patents in the U.S. but had little to show for it. Developing OnStar, a phone signal transmitted by the car, GM never took full advantage of this cellular phone tech in its vehicles:

Musk had proven that such a connection could be used for so much more. The Tesla Model S could have its software updated remotely that way, or through the user’s home wireless internet. This allowed engineers and programmers to make improvements to the sedan after it was sold, without necessitating a burdensome trip to the shop. A part, for example, might be wearing out, but it could be saved by programmers if they changed the car’s code to reduce the torque applied to it. This ability became critical for Tesla in the fall of 2013, when a string of Model S fires began raising concerns about the safety of a vehicle with thousands of lithium-ion cells onboard. The first fire occurred in October, near Seattle. A Model S ran over debris on the road that damaged the underside of the car, puncturing the vehicle’s battery pack [legitimizing Peter Rawlinson’s earlier concern, back when he and Musk had fought over millimeters of car height].

[Kindle Location: 3,095]

Tesla even used the technology to raise the height of their cars which made it less likely for their batteries to puncture:

Tesla’s engineering team got moving. As they studied the fires, they realized that the car’s low height off the ground increased the statistical likelihood of running over something that would puncture its batteries. Thousands of other cars might pass over the same road debris, but because their underbodies sat fractions of an inch higher, the odds of damage dropped dramatically. Tesla engineers calculated that if they used the car’s suspension to lift the body up just a smidge, the chances of striking debris would be reduced. They changed the software and sent it out to the fleet that winter. It worked, buying them a few months to come up with a thicker plate to protect the battery pack. In the meantime, reports of car fires quickly disappeared.

[Kindle Location: 3,113]

It’s a stretch to say GM’s failure to use cell tech for service and repairs is solely because GM franchise dealers rely on service for a large part of their gross profit. But there are strange incentives linked to GM’s outdated wholesale model.

Legacy carmakers noted that Tesla wouldn’t be able to service customers without franchise dealers but Tesla used innovation in this area. Trying to keep customers happy in Norway with a limited budget for service locations, Tesla figured out that 90% of Model S service issues can be identified remotely and 80% of fixes can be done at the home or office of the car’s owner.

What wasn’t said was that McNeill was going to have to find ways to improve the customer experience beyond just hiring a bigger staff and opening more stores and service centers. Tesla didn’t have the money for what would be truly needed once the Model 3 arrived. Instead, his team began looking at the data coming off the Model S and realized they could identify 90 percent of the service issues remotely and fix 80 percent at an owner’s home or office, including seat replacements and brake repairs - basically everything but replacing batteries and drivetrains. Instead of spending millions to build more service bays, McNeill’s team would put hundreds of technicians into service vans to make house calls.

[Kindle Location: 3,611]

Valuation

The September 2020 McKinsey report explains why it is hard for legacy carmakers to switch to the direct-to-consumer or “OEM owning retail” approach:

The “OEM owning retail” approach integrates all retail activities into the hand of the OEM and implies the highest level of control and customer access, but also high investment needs in its own physical outlets. While we see traditional OEMs moving away from their own retail activities, new players like Tesla or NIO are leveraging this approach to build a lean and asset-light network of highly differentiated physical stores around an online backbone.

Prerequisites: In the short term, this model is primarily viable for new players with no existing network structures or traditional players entering new markets.

For OEMs: This model requires OEMs to make heavy investments into brick-and-mortar retail locations. To make this feasible, they will need to grow online sales quickly in order to reduce the capex requirements of building and running a dense network of physical outlets.

For customers: If managed successfully, this approach could enable a distinctive and seamless experience for customers - in turn, putting OEMs in the perfect position to gradually move to an online-only sales model. Additionally, fully owned sales and service formats provide a more tailored or even personalized experience for customers.

This challenge for legacy automakers is one of the reasons why Tesla’s valuation appears high on a relative basis.

Having a direct relationship with customers, Tesla offers a monthly full self driving subscription. Given the way they are closely connected to customers, I expect Tesla to have other monthly offerings in the coming years and this can be very valuable.

If we posit that the bulk of the free cash flow for Toyota (TM) will come from electric cars over the next 50 years and that they’re just getting started while Tesla is already on pace to sell over 1 million EVs in 2022 then it doesn’t seem unreasonable that Tesla’s enterprise value is 2.5 times higher than Toyota’s. Of course many people don’t see it through this lens; they anchor on a lens that sees Toyota’s sales of nearly 10 million non-electric cars per year.

Regarding the Tesla numbers above, I get a market cap of $1,072 billion based on 1,004,264,852 shares outstanding as of October 21st times the December 23rd share price of $1,067. Their enterprise value is roughly the same as their market cap.

The Toyota 20-F through March 2021 says each ADR represents 2 shares of common stock and the 2Q22 financial summary says the following:

On October 1, 2021, TMC effected a five-for-one stock split of its common stock to shareholders of record as of September 30, 2021.

As such, my read says each ADR is worth 10 shares after the split. The average number of shares outstanding through September was 13,973,124,493 which equates to 1.4 billion ADRs so I get a market cap of $257 billion for Toyota based on the December 23rd ADR price of $183.78.

Toyota’s enterprise value is higher than their market cap due so the following from their 2Q22 financial summary through September 2021:

¥13,864,894 million long-term debt

¥10,754,902 million short-term debt

¥881,989 million non-controlling interests

¥ (4,954,834) million cash and equivalents

--------------------

¥20,546,951 million

Using an exchange rate of 1 Yen to 0.0087 USD, this comes to an amount of nearly $179 billion over the market cap of $257 billion such that the enterprise value is $436 billion.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Long TSLA, AAPL, GOOG, GOOGL, VOO