Iteris and the Roadway Sensor Industry

Iteris and the Roadway Sensor Industry

Analyst: Young Money Capital

Investment Thesis

Roadway sensors have a large TAM that is quickly growing due to serious safety, economic, and environmental concerns. Iteris (ITI), a roadway sensor company, has the dominant market share in the industry. They have signalized over 1/3rd of all traffic lights in the United States. The U.S. Government trusts Iteris’s systems over their competitors. Iteris has a large moat from its scale and reliability. Their scale allows them to have the most data, thus, the most accurate predictive analytics. This reduces casualties, money, and pollution. Iteris will benefit from multiple tailwinds including the Biden Administrations’ recent infrastructure bill. Their net bookings also suggest an acceleration in revenue. Iteris has a long runway because there are millions of traffic lights worldwide that are not signalized.

Industry Analysis

Traffic accidents cost the US nearly 1 trillion dollars a year. Of these traffic accidents, federal and local governments pay for 7% of them. Fifty percent of accidents happen at intersections.

Iteris’s sensors capture data around cars, bikers, and pedestrians and adjust traffic light timing to reduce accidents and save people time. At one intersection in Tampa Bay, Iteris prevented 15-25 close calls per day saving lives. In another case study from Orange, Calif, Iteris’s traffic synchronization program reduced travel time by 13% saving time. Reducing travel time also reduces fuel costs. Congestion wastes 3.3 billion gallons of fuel per year which equates to approximately $13 billion in wasted gas and 29 million metric tons of carbon dioxide. The reduction in travel time saved residents’ gas and reduced pollution.

New Funding

Source: Iteris Investor Relations

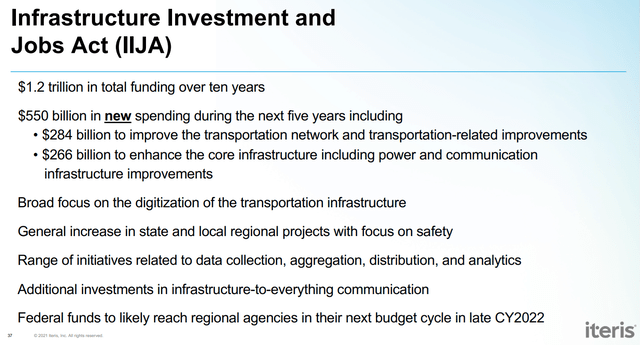

Recently, the Biden Administration passed the $1.2T Infrastructure Investment and Jobs act. The increase in federal funding for infrastructure and transportation will be a tailwind for Iteris. Iteris’s strong government relations segment has allowed them to be a part of coalitions deciding the allocation of funds for the II&J act,

“We're actually affiliated with a coalition that is working closely with the National Safety Council. That's actually a relatively small amount of funding. The initial funding is $1.5 billion … that's just an example of one activity that we're closely engaged with key sponsors, and that's quite topical because it's been in the news lately.”

California is a great example of how Iteris will benefit the infrastructure bill. California wrote a high-level analysis of how they will spend the funding and they mentioned improving “congestion” fourteen times. The infrastructure bill included 13.2 billion for congestion mitigation and air quality improvement and 250 million for the congestion relief program to be spent over five years.

Iteris management predicted that the funds will reach local agencies (i.e. Iteris’s customers), in late 2022 and be spent on projects then, providing a tailwind.

Competitive Advantage

Iteris has the dominant market share in the roadway sensors and transportation services industry. In 2020 Iteris, “designed, deployed, or equipped >33% of all signalized intersections in the US.”

This quarter, Iteris has continued to take market share.

Iteris’s competition mainly consists of companies that have focused outside of signalized intersections. To install radar vehicle detection, a company needs to be on a qualified products list. Iteris is the only company to be on California, Texas, and New York state’s qualified products list. Only two companies are on the New York qualified products list, four on Texas qualified list, and four on the California list creating a barrier to entry. Iteris is the only company on all these lists.

Iteris’s Data Advantage

Source: Iteris Investor Relations

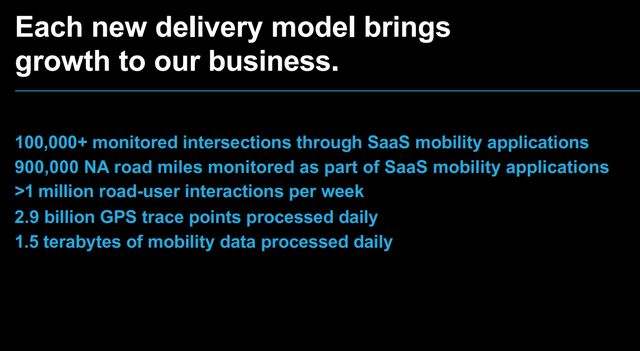

Iteris has a series of moats that protects their competitive advantage and enables their large market share. Their superior scale enables most of their advantages including data, connectivity, and trust. Iteris monitors more than 100,000 intersections and processes 1.5 terabytes of data daily. With more data, Iteris’s predictive analytics and object identification improve, thus, creating a more valuable offering. Iteris’s competitors do not have enough sensors to collect as much data. Iteris has 32 patents protecting its technology.

Also, Iteris times their traffic lights with other lights in their system creating smoother traffic flows. It would make sense for neighboring towns to use Iteris so that they could link up their traffic lights. As more traffic lights come onto Iteris’s system, the system becomes more valuable.

Government employees are notoriously risk-averse. Since Iteris is a known quantity, government employees would rather hire Iteris than take an unnecessary risk on an upstart. As more cities hire Iteris, their brand name continues to improve.

Iteris’s competitive advantage is further shown by their closest competitor, Rekor, trying to buy them out for a 37%-43% premium.

Rekor cannot build the network Iteris has so they tried to buy it. Iteris’s management showed faith in the company and declined the offer.

Optionality

Source: OpenStreetMap

Iteris has geographic and product optionality. Iteris is primarily located on the West Coast, Texas, and Florida. Iteris management stated that the Northeast is a “big focus”.

The northeast has a high density of intersections so expansion there makes sense.

The global number of traffic lights is “well into the millions” so Iteris still has a giant runway that they could expand.

Iteris also has product optionality. Iteris has joined the Mobility Transformation Center as a founding partner alongside Ford, Nissan, General Motors, and Toyota. They are part of a leadership group focusing on automated vehicles and connecting vehicles to avoid crashes. Iteris could be a potential acquisition target for companies trying to get into the self-driving vehicle space.

Management/Use of Cash

Joe Bergera has been the CEO of Iteris since 2015. He has made a small acquisition at an interval of every 12-18 months but has shown reluctance to do so with the stock trading under $4. In 2020, he also divested the agriculture and weather segment.

Insider Transactions

Source: Market Beat

Insider transactions have been favorable in the past six months for Iteris. No one has sold and insiders have bought. It makes sense as net bookings are accelerating and Iteris is about to have a tailwind from the infrastructure bill.

Risks

Iteris’s main risk is in their one-time expenses. They blamed a one-time write-off and supply chain issues for their margins deteriorating. Specifically, their contract with Iowa cost them.

“While it didn't impact revenue in the period, we did take a write-off in the second quarter of $2.8 million for one of our service lines… Additionally, I want to confirm that we do not have any other contracts with similar terms. This was a very unique contract and we've certainly learned several lessons from this experience.”

If it was not for this contract, gross margins for services would have been in the 35% range consistent with prior years.

Management also blamed supply chain issues and stated that it pressured revenue and margins.

“Although we continue to anticipate elevated supply chain costs for the next few quarters, this will be better offset by higher sales volume and other mitigations beginning in the fourth quarter, including the price increases that we mentioned. As a result, we anticipate a fourth-quarter improvement in gross margin and operating leverage”

The risk is that these are not one-time issues. If these issues continue to come up then Iteris’s margins will deteriorate. This risk is low as managements reasoning makes sense.

Valuation

Revenue Drivers

Source Author data from SEC Filings

Iteris has one quarter left in the fiscal year 2022. Iteris’s product and services revenue is projected to accelerate in 2023 due to Iteris’s record high backlog, easing of supply chain issues, and the tailwind from the infrastructure bill. Gross margins for services should return to normal in 2023 after the one-time write-off and expand due to the shift to recurring SaaS revenue.

Margins

Source Author data from SEC Filings

As supply issues subside, they should be able to continue to expand operating margins as Iteris is a monopoly with pricing power. The big jump in normalized Depreciation and Amortization is from their failed Iowa project which includes a large one-time expense. It is expected that Iteris will see some multiple compression, but it will be slow as they do have a strong moat. Using the above assumptions, Iteris will have an IRR of 26.7%.

Disclosure: I/we have a beneficial long position in the shares of ITI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.