Netflix's Biggest Competition is Still "Sleep"

Young Money Capital

Investment Thesis

Growth in the streaming industry is still in the early stages of the S-curve. There are over a billion paid cable subscribers and only 214 million Netflix subscribers. While the US market is close to saturated, Netflix will be able to add subscribers from Asia and eventually Africa. Netflix will return to adding 30 million subscribers per year after the covid “pull forward”. Netflix’s churn rate of 2.4% is low, suggesting that customers are satisfied with their service level and Netflix has future pricing power. When Netflix raises prices, revenue increases will go straight to the bottom line because of Netflix’s operating leverage. Reed Hastings, Founder, and Co-CEO is still with the company delivering his vision. Netflix has limited competition as Disney+ and Hulu are not real threats which will be discussed later.

Industry Overview

3rd Quarter Netflix Shareholder Letter Quarterly Earnings

Streaming is a disruptive innovation that is better than cable because it is cheaper, wireless, and on-demand. This is further evidenced by many cable channels launching streaming services. Trying to drive traffic to their streaming service, many are creating exclusive content for their streaming service, thus, weakening their cable tv offering. Weaker cable content will be a tailwind for all streaming services; while continuously taking market share, streaming has only a 28% share of total US tv time (see chart above). Streaming’s low market share shows a long runway for growth as the industry continues to mature.

In the premium SVOD streaming industry, three companies dominate; Netflix, Hulu, and Disney+ each have a respective market share of 31%, 20%, and 17%. There are other smaller competitors, but the focus of this article will be on Disney+ and Hulu. Neither Hulu nor Disney+ is a serious threat to Netflix. Disney, one of Hulu’s biggest competitors, owns 2/3rds of Hulu while Comcast owns the other 1/3rd creating a misaligned competitive structure. Disney would rather Disney+ be successful because they own all of it, unlike Hulu. This is evidenced by Disney removing content from Hulu and putting it on their streaming platform weakening Hulu’s product offering.

Streaming Giants' Next Worry: A Subscriber Churn Uptick

Disney+ had a lot of support around its launch and quickly added subscribers from their pre-existing fanbase. Then Disney+ made the bold claim that they would have 230-260 million subscribers by 2024, more than Netflix’s current subscribers. Despite what management claims, Disney+ is also unable to compete with Netflix. Disney+ growth has slowed significantly as they added only 2.1 million subscribers last quarter. Even worse, this is with a lower price point than previous quarters. Disney+ paid subscribers average per subscription is currently $4.12 decreasing from $4.52 while having historically higher churn than Netflix. Netflix added 4.4 million subscribers last quarter and they are forecasting 8.5 million next quarter. Netflix’s growth comes despite increasing prices and their average price point is nearly tripled Disney+. Netflix’s average revenue per membership is up 5% year over year excluding foreign exchange impact to $11.61. Netflix has higher growth, lower churn, and a higher price point than Disney+. Disney+ and others should be able to carve out a niche in the industry, but Netflix will take the majority of the industry.

Competitive Advantage/KPIs

Netflix’s competitive advantage rests on its scale, recommendation engine, and original programming. As Netflix adds subscribers and raises subscription prices, it drives revenue. They can spend that money on more content continuously building their library. As their content library grows, customers’ willingness to pay increases, creating a flywheel effect. The large upfront costs, time, and expertise bar any new entrants from entering the industry. Even established legacy players, such as Disney, are having a hard time keeping up with the amount of content Netflix is putting out. Netflix is also benefitting from the success of dubbing in international markets. From 2020 to 2021, dubbing consumption has grown by 120%. Content produced for one region is often successful in multiple regions as evidenced by Netflix’s hit Squid Games. The success of dubbing increases the value of pre-existing content. The importance of scale makes streaming a winner-takes-most industry.

Netflix was the first streaming company that enabled them to build the best recommendation engine. Netflix’s recommendation engine is a machine learning application which means that with more data it continuously improves. Netflix started its recommendation engine years before it entered streaming, enabling them to collect more data than its competitors. Netflix also has more subscribers which produces more data. No competitor has as much data as Netflix does and the lead is widening. The advantage is used in two different ways. Netflix can buy low-cost niche shows and find the perfect audience for the show to become popular. Netflix also uses the data to tell directors what shows will be successful. Netflix maximizes its content better through its recommendation engine.

Netflix used to be known for cheap low budget niche tv that was optimized by their recommendation engine. Over the past few years, Netflix has invested heavily into their Los Angeles and Albuquerque studios for making their original content a success. Their original content received “the most Emmys ever for any single network or service in a season of television, with 44 (tying CBS’ tally in 1974 when there were only three national networks).” (Q3 2021 Letter to Shareholders). Now the criticism for Netflix’s content is their lack of hit movies. In their most recent earnings call, Netflix responded by saying “Well, remember, we're a few years behind in the film business, the way we -- from our TV business when we started making meaningful budget original film about 3 years ago. So -- and in that time, we've had 5 Oscar-nominated best pictures and some big, big films in terms of viewing… I think it's interesting that, that's going to continue to grow.” (Theodore A. Sarandos Q3 2021 earnings call). Given time, Netflix’s movies will catch up to its already premium tv shows.

Netflix’s key performance indicators are subscription growth, customer acquisition cost, churn rate, and average revenue per membership. Netflix should be able to continue their long-term average growth of about 30 million subscribers per year after the covid pull forward because of their long growth runway. Management is projecting 8.5 million subscribers next quarter slightly ahead of the 30 million annual pace. This number is closely related to their customer acquisition cost.

Source: Created by Author data from Netflix Investor Relations

Netflix’s customer acquisition costs include marketing costs, increase in content assets, and amortization of old content assets. Covid, in 2020, allowed Netflix to acquire customers much cheaper than in the past and now Netflix is facing the pull-forward headwinds making it more expensive currently. These headwinds are projected to subside next quarter. Factoring in the ~8% pricing increase Netflix announced on 1/14/2022, Netflix’s customers spend $150 per year on average. Assuming a monthly churn rate of 2% (subscription services have lower churn rates as they mature), a long-term pricing increase of 3%, and an 8% required IRR a Netflix customer is worth $567. This number is understated because it does not include Netflix’s more aggressive short-term price hikes. Netflix is efficient in acquiring customers compared to their CAC with the exception of the 2021 abnormal Covid pull forward year.

Netflix’s churn rate and average revenue per membership are two key inputs into the value of the customer. Raising prices often raises the churn rate as people cancel their subscriptions. Fortunately, Netflix has not had this happen. Netflix has raised its average revenue per membership since 2019 and has kept its churn rates below 3% even during the Covid pull forward. (see graph above). This shows that Netflix has pricing power and should be able to continue to raise prices in the future. The increase in prices with a similar churn rate will allow Netflix to increase the value of their customer, increase their margins, and generate meaningful free cash flow.

Optionality

Netflix has geographic optionality and product optionality. Netflix is currently hyper-focused on expanding into Asia (excluding China). Reed Hastings was famously quoted as saying his next 100 million subscribers were going to come from India. Asia is a large, mostly untapped market for Netflix as they only have 30 million subscribers from the region. Netflix has the opportunity for future expansion in Africa when the infrastructure in the region catches up.

Netflix is also moving into interactive tv and e-commerce. Netflix is trying to engage subscribers more as they are competing with distractions such as the phone and video games. Their interactive tv captures the viewers’ attention more. Netflix is going to launch stores on the app so super fans can buy their favorite show’s merchandise. This is another angle where Netflix will be able to boost revenue.

Capital Allocation

Netflix has been approximately free cash flow breakeven for the past two years. Netflix is using all of its cash to produce more content to bring in new subscribers. This is a smart use of cash because of Netflix’s efficiency where their CAC is lower than their total value of the customer. As long as Netflix continues to acquire customers efficiently, then they should use their cash on content and marketing.

Valuation

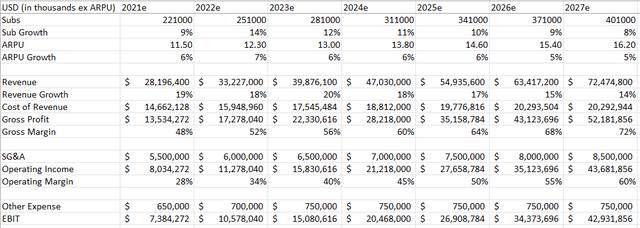

My philosophy for valuation is to simplify everything. This allows me to see the leverage in the industry and better track what metrics drive the stock price. I normally focus on revenue drivers, gross profit, and EBITDA and compare it to the enterprise value to standardize for leverage. Netflix amortizes the majority of its content in the first year, so I believe EBIT is a more appropriate valuation metric than EBITDA. I do not factor in interest because it is already factored in the enterprise value. I also choose not to factor in taxes because taxes should normalize between companies over a long enough time horizon. This allows standardized comparison between companies. I forecast six years out because growth companies are trading in the future not today. Netflix is growing fast, but they are not a hyper-growth company so I believe a 10X exit EV/EBIT multiple from their 2027 earnings is appropriate which would value the company at an enterprise value of $429 bn which is 42% above their current enterprise value of $302bn (as of 12/2/2021). Below are Netflix’s historical statements and forecasted statements. This model does not include their e-commerce optionality. If that becomes a big hit Netflix could be worth more.

Source: Created by Author Data from Netflix

Disclosure: I/we have a beneficial long position in the shares of NFLX either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Edited 1/15/2022