Sea Limited's Growth Opportunities Are Not Priced In

Sea Limited's Growth Opportunities Are Not Priced In

Analyst: Young Money Capital

Investment Thesis

Sea Limited (SE) is an undervalued investment. The shift of retail sales to e-commerce is just beginning with a global penetration of around ~20%. Southeast Asia and LATAM are under-penetrated and growing faster than the rest of the world. The underlying shift to mobile-commerce (m-commerce) will be a tailwind for Sea Limited because they dominate mobile shopping. They successfully turned shopping into a game creating community and brand loyalty to their platform. They have scale advantages over their regional competitors. They have a long runway to reinvest into new regions and territories and their video game business produces strong cash flow allowing their e-commerce business to take a loss-leader approach. Sea Limited is founder-led and the CEO is only 44 years old.

Company Overview

Sea Limited is a conglomerate based out of Singapore. The company has four main business segments: Shopee (E-commerce), Garena (Video Games), SeaMoney (Fintech), and other bets. Sea Limited started as a video game company in 2009 and founded the segment Shopee in 2015. Garena is the only profitable segment of Sea Limited’s business that funds the growth for the other segments. Shopee takes Garena video game ideas and gamifies online shopping. Shopee has grown to be the most valuable part of Sea Limited’s business. This report will first focus on Shopee, then discuss Garena, followed by SeaMoney. Limited data is available on Sea Limited’s other bets as they do not break them out into separate segments.

Shopee

Industry Analysis

The e-commerce industry is attractive. Digitalizing sales is a capital-light business with increasing penetration from the traditional brick and mortar industry. Shopee’s e-commerce platform started in the Southeast Asian region. In October 2019, Shopee launched in LATAM, and in 2021 they launched in selective parts of Europe and India. In the southeast Asian region, Shopee has 57% gross merchandise value (GMV) of the total E-commerce industry.

Southeast Asia’s e-commerce industry’s growth prospects are particularly strong. Southeast Asia e-commerce only has a 13% penetration of total retail sales in 2020 showing its long runway (more recent data was unavailable). By 2025, Southeast Asia’s e-commerce industry is expected to grow at a CAGR of 18% compared to the US’s 7.7%, nearly 2.5 times as fast.

Shopee Market Share by Region

Source: Punch Card Investor

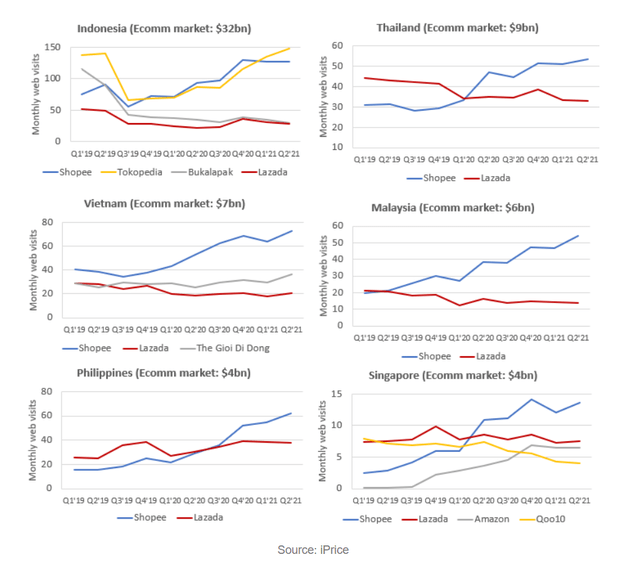

Sea Limited’s largest competitors in Southeast Asia are Lazada, Alibaba’s (BABA) e-commerce segment, and Tokopedia, a regional player in Indonesia. Lazada is not a large threat to Sea Limited. Lazada has been losing consistent market share in almost every region. In addition, Lazada's poor relationship with the Chinese Government is not helping.

Shopee Returns to MAU Growth in Indonesia

Source: Punch Card Investor

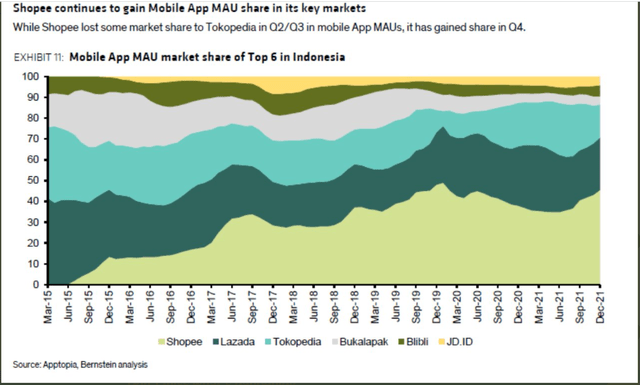

Tokopedia is a regional Indonesia e-commerce platform and Shopee’s toughest competition. Concerningly, Tokopedia took market share from Shopee in Q2 and Q3 of 2021. Alternative data suggests that the trend reversed in Q4 because Shopee increased its market share of mobile app monthly active users (MAUs). It seems like Shopee has the upper hand in Indonesia because of its scale advantage, however, data is limited because Tokopedia is not a public company.

LATAM E-commerce is Expected to Triple

Source: Lazard Asset Management

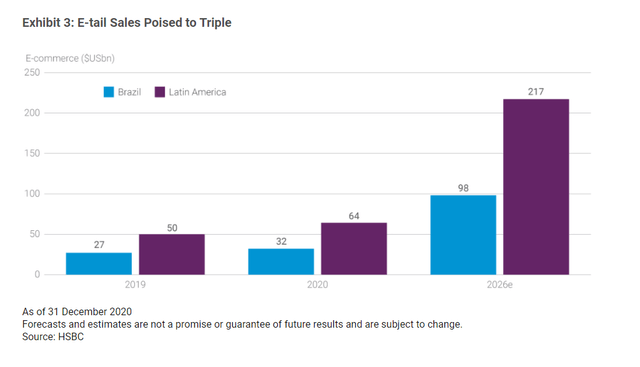

Shopee launched in 2019 and is a newer player in the LATAM e-commerce region. The LATAM e-commerce market is another positive for Shoppe. In 2020, the market penetration is also 13% of retail showing a long runway for growth (more recent data was unavailable). The market is supposed to more than triple from 2020-2026.

Source: Apptopia

Despite recently launching, Shopee passed Mercado Libre (MELI) in market share by MAUs. Shopee is known as a mobile-first e-commerce platform. In 2021, half of LATAM sales will be mobile, however, by 2024, 75% will be mobile. This creates a strong tailwind for Shopee in the LATAM region.

Competitive Advantage

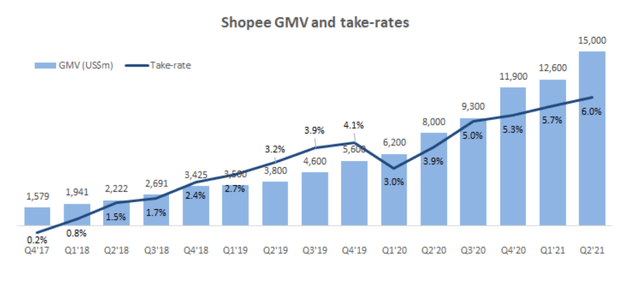

Shopee has used the same successful strategy to launch into new regions. They use a loss-leading strategy to gain market share in the new region. They set a low take rate and spare spend heavily on advertising. A take rate is the percentage of the GMV that the platform gets to keep as opposed to the shop. This creates network effects with the addition of new consumers and shops on their platform.

Shopee can lose money short term in the search for growth due to Garena’s strong profitability. Shopee sets take rates low to incentivize consumers and shops to come onto their network. In Brazil, LATAM’s biggest and most valuable e-commerce market, Shopee now has the most monthly active users and has “more than one million local sellers in Brazil have registered with Shopee since we started welcoming local sellers in mid-2020,” (Q3 Earnings Call SE). Consumers get more stock-keeping units (SKUs) to choose from and shops have more consumers to sell to strengthen the network. This loss-leading strategy cannot be easily repeated by regional competitors as they do not have a cash flow positive segment supporting their e-commerce business.

Shopee has been known to hire local celebrities for their launch to foster brand loyalty and acquire people to their network. In their LATAM launch, they hired famous soccer player Christiano Ronaldo as a spokesperson and were known to blanket train stations with their advertisements. They then used expertise from Garena to gamify the shopping experience. This made shopping on their platform social and cool. The gamification of their platform was recently rolled out to sellers too. “We recently launched a Seller Mission, an incentive program that rewards sellers with privilege as they complete certain tasks. The program gamifies the experience of sellers as it guides them through features and tools on Shopee that they can use to become better sellers,” (Q3 Earnings Call SE). It is no surprise that in 2021 Shopee ranked as the sixth-best brand globally by YouGov.

Source: Punch Card Investor

Once Shopee gains a strong market position, it can slowly raise take rates. Malaysia and Thailand became their first two regions to become EBITDA positive suggesting the strategy is working. In Q2 2021, their take rate averaged a 6% take rate which is considerably lower than more established e-commerce players. Amazon averages a 15% take rate not including value add services like fulfillment, shipping, and inventory fees.

Optionality

Sea Limited has geographic optionality in its e-commerce business. In late 2021, Sea Limited launched in Poland, France, Spain, and India. While it has only been a few months since the launch, the results have been positive so far. It is also important to watch Shopee in Poland. Poland is the first region between primarily Amazon and Shopee. Shopee could expand into more countries in the future further lengthening their growth runway.

Garena

Industry Analysis

The video game industry is highly volatile. Games have high upfront costs and lots of uncertainty in how profitable they will become. Video games often have a short shelf life because gamers get enticed by the next big game. Brand loyalty is extremely difficult to come by, however, highly profitable. When video games have high brand loyalty, they have large margins and high ROIC as the costs are mainly fixed. The ultimate success is a video game franchise. An example of this is "Madden Football" which annually produces a hit game that its loyal fans buy. Garena has one main game, "Free Fire", making the segment risky. Bulls say Garena’s "Free Fire" is a franchise and bears argue that it is a one-hit-wonder.

Competitive Advantage

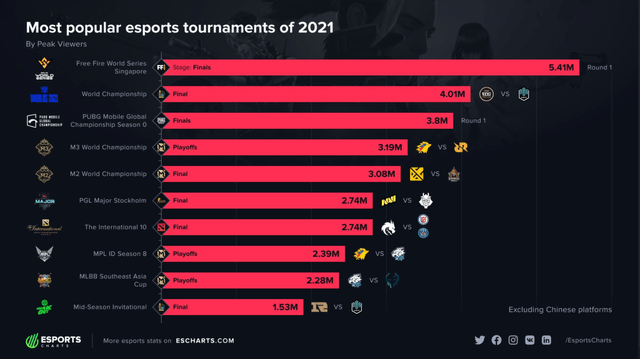

E-Sports Tournament Streaming

Source: Max Bosenko

Garena’s "Free Fire" franchise has strong customer loyalty. Garena has created professional gaming tournaments for "Free Fire". They broke a record for most people concurrently streaming a video game event with 5.4 million viewers. The next closest video game event only had 4 million viewers. On top of that, "Free Fire’s" theme song “has been streamed over 50 million times across various online platforms to date.”

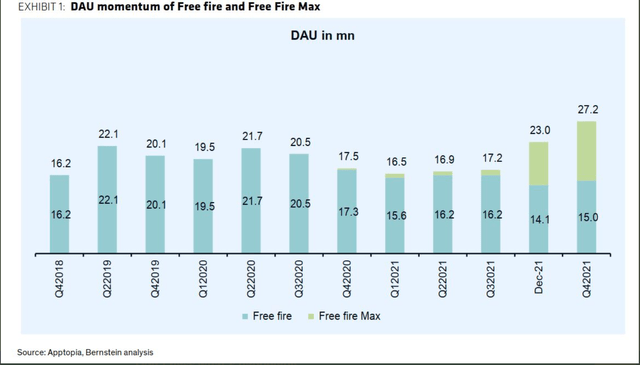

DAU Returns to Growth

Source: Mr. Buyside

In late 2020, early 2021, an extremely concerning trend appeared for Garena’s "Free Fire"; a franchise with supposable strong customer loyalty. Despite revenue increasing, daily active users (DAUs) were decreasing suggesting the game was getting stale. This trend reversed as Garena released its next iteration of the "Free Fire" franchise called "Free Fire Max". Between the two games, DAUs are now at an all-time high. In addition, the "Free Fire Max" franchise allows for additional monetization compared to the "Free Fire" game. "Free Fire" has a solid competitive position, but it is far from an impenetrable moat. It is up to management to continue to execute and grow the business.

SeaMoney

SeaMoney is Sea Limited’s fintech arm. SeaMoney is a mobile wallet that is integrated with Shopee and Garena. The segment accounted for 4.6 billion in total payment volume and 132 million in revenue in the third quarter. SE Investor Relations. The revenue increase year over year is 818%. Q3 Sea Limited Earnings Report. SeaMoney is becoming large enough to have an impact on Sea Limited’s top-line growth. SeaMoney also helps strengthen Sea Limited’s competitive advantage. Having their mobile wallet strengthens their ecosystem for both Shopee and Garena.

Management Team/Capital Allocation

Sea Limited has two key executives: Forrest Li and Chris Feng. Forrest Li is the founder and CEO of Sea Limited. He owns 24.2% of Sea Limited aligning his incentives with shareholders. He is 44 years old suggesting he will run the company for a long time. Historically, founder-led companies have outperformed non-founder-led companies. Forrest Li takes the lead on the Garena division.

Chris Feng is the CEO of Shopee and SeaMoney. Before working at Shopee, Chris Feng worked at rival Lazada. Chris Feng is credited with the rise of Shopee and SeaMoney. He is 37 years old.

In September, Sea Limited raised about $6 billion from an equity share issuance. Normally, equity share issuance is an indication the stock could be overvalued as management is trying to make the share price “real”. Sea Limited’s management team stated the equity issuance will fund e-commerce expansion into Poland, France, Spain, and India. If Sea Limited’s return on investment is high enough from the new regions, it could be worth the share dilution.

Risks

Investing in Sea Limited does not come without risks. Sea Limited trades at a relatively high valuation and a slowdown in growth will hurt the stock. Many bears claim that Sea Limited will see an increase in competition. Sea Limited's competitive advantages discussed earlier should be enough to hold off competition. The key performance indicators (KPIs) GMV growth rate, take rate, and period average active users growth rate will need to be tracked to ensure their competitive advantage is still intact.

Valuation

Source: Author historical data from SE Investor Relations

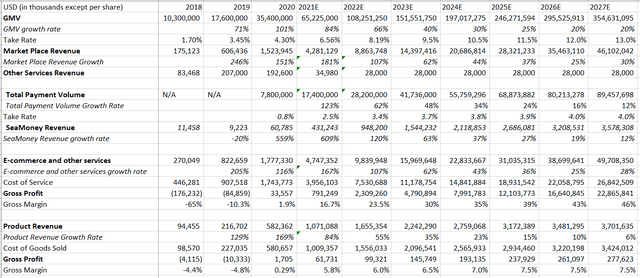

The above graph is the revenue drivers for the E-commerce and Shopee section. The top section grouping is the drivers for the 3rd party Marketplace. The world E-commerce market is projected to decelerate after the 2021 covid pull forward effect. E-marketer projects the world E-commerce GMV growth rate will be 75% of the previous year. Since Shopee showed above market average resilience in the 2020-2021 e-commerce slowdown, Shopee GMV is projected to be slightly higher than the 75% deceleration. As Shopee reaches market saturation, GMV is then projected to slow down to near the industry average. The take rate is projected to expand to be closer to the industry leader, Amazon. Amazon currently has a 15% take rate before value-add services. It is reasonable to project Shopee to have a 13% take rate, not including value-add services in 2027.

In the next section, SeaMoney’s total payment volume (TPV) is projected to increase, but at a decelerating rate. It is questionable how much pricing power SeaMoney will have to raise their take rate so the estimate is conservative. SeaMoney’s does provide ecosystem control enhancing Shopee and Garena’s competitive advantage. Unfortunately, Sea Limited does not break out SeaMoney’s cost of service expenses from Shopee 3rd party marketplace. The section below is their combined expenses. In the last section, Shopee’s 1st party market product revenue is shown. Since Shopee’s focus is on the more valuable 3rd party revenue, their revenue is projected to slow considerably.

Source: Author historical data from SE Investor Relations

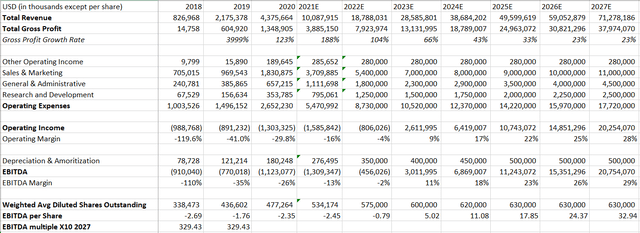

This graph is for Garena’s revenue drivers. Early indicators show that Garena’s growth slowdown from Q3 2021 is returning to normal. Growth is supposed to quickly slow down thereafter as the market reaches saturation. Early indicators show Free Fire Max is better at monetizing than the original Free Fire, so the average revenue per user is supposed to increase as well.

Source: Author historical data from SE Investor Relations

As Sea Limited’s revenue rapidly grows, their margins will expand because of their high fixed costs. Their share dilution will slow in 2023 as they become profitable. They will not need to dilute themselves as they will have sufficient cash for reinvestment. A 10x 2027 EBITDA multiple is appropriate for Sea Limited because they have some high growth segments (Shopee), but the rest of the company’s growth will slow considerably. The stock is fairly valued at $329 which implies considerable upside from its current price of $187 (as of 1/7/2021).

Disclosure: I/we have a beneficial long position in the shares of SE either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Edited 1/11/22