Zebra: The Industry Leader in Warehouse Automation

Zebra: The Industry Leader in Warehouse Automation

Analysts: Young Money Capital and Fiducia Invest

Note: This article on Zebra is co-authored by Fiducia Invest and Myself. Fiducia is a very smart investor and has his own website full of research that can be checked out here.

Business Overview

Segments

Zebra operates in two segments: Asset Intelligence & Tracking (AIT) which accounts for ~30% of total revenue and Enterprise Visibility & Mobility (EVM) which accounts for ~70% of total revenue. The AIT segment consists mainly of manufacturing and selling barcode printers, which print barcodes, plastic cards with radio frequency identifier RFID tags, and other identifiers to track products. The EVM focuses on handheld devices to scan these barcodes and tags and software to optimize and automate workflow. The two segments are vertically integrated and highly correlated with each other. Management stated in the last earnings call “The growth between AIT and EVM is actually quite similar. It's not materially different. EVM would likely have a slightly higher growth rate, but not materially so.”

Zebra Segments

Source: Zebra SEC Filings

Example of each vertical

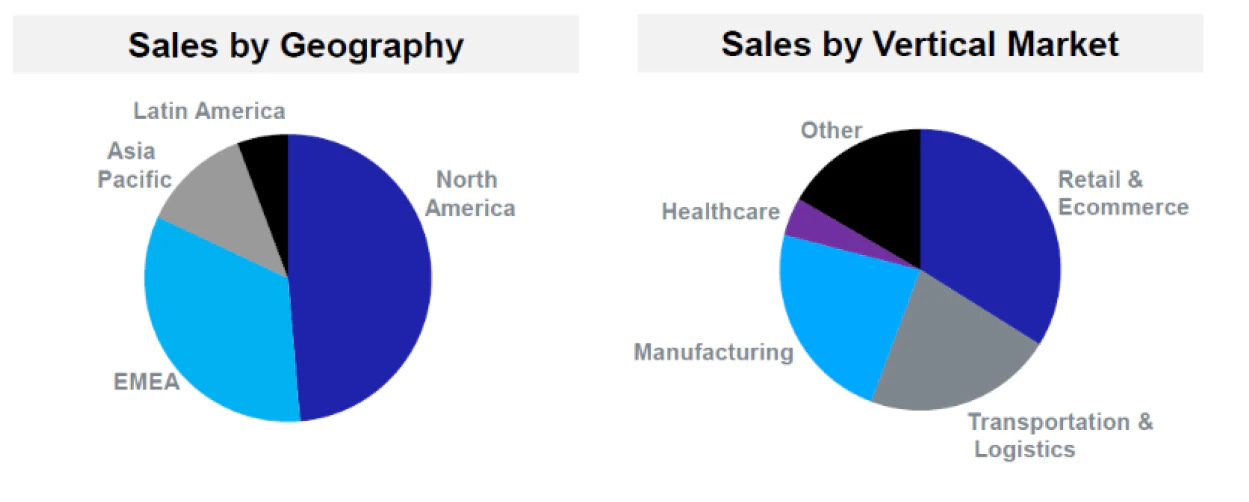

Zebra has various verticals, these include Retail and E-commerce, Manufacturing, Transportation and Logistics, Healthcare, Public Sector, and Hospitality.

Mass merchant, grocery, and e-tail subsectors are about 2/3 of Zebra’s sales in the Retail and E-commerce segment. The adoption of omnichannel and e-commerce has sped up this vertical due to COVID-19. Associates will have a mobile computer and track and trace assets from production to the shelf. Currently, only ⅓ of retail store associates have a form of a mobile device, Zebra claims that every worker needs one. Transportation & Logistics is critical as well, with an increased e-commerce presence and omnichannel with customers such as Amazon, Home Depot, and Target. Manufacturing (food, pharma), discrete manufacturing (aviation, electronics auto), are another component of Zebra’s revenue stream and this allows for intelligent automation and increased automation in workflows for sensing and tracking (track and trace from production to shelf). The last sizable vertical is healthcare, which accelerated post COVID-19 for mobility, contact tracing, and remote patient care. Hospitals can also keep track of inventory utilizing RFID technology.

Breakdown of verticals (revenue % chart)

Source: Punch Card Investor

Industry

E-commerce Trends

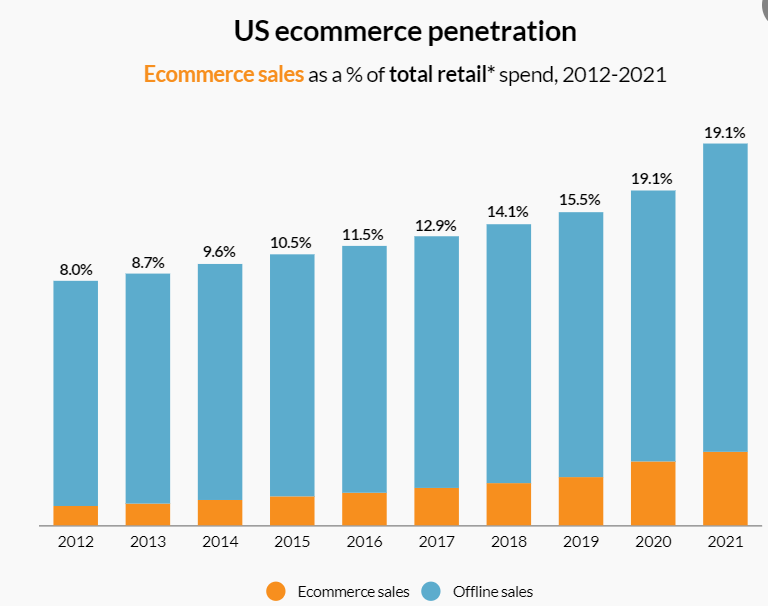

The shift to e-commerce is an industry trend that Zebra will directly benefit from as 1/3rd of their revenue comes from the Retail and E-commerce segment. As consumers order more stuff online, a larger focus will be on optimizing warehouses for shipping. Currently, only 19% of total US sales are online, but that percentage has been consistently growing.

Source: Digital Commerce

Automation trends

There are two types of automation trends: Digital automation, which relies on software to reduce manual processes, and physical automation, which is the automation equipment used to reduce employee labor. There are stark benefits of warehouse automation, and a bright spot in labor expenses. According to the US Bureau of labor statistics, an average warehouse costs $3.7m in annual expenses. This does not include health insurance, overtime, unemployment, etc. Lowering expenses to the business is a big benefactor of warehouse automation. Adopting automated systems can help reduce human error, minimize human labor, improve workplace safety, boost inventory control, and also improve customer service.

WMS, or warehouse management system, is the backbone of tracking inventory, directing picking and packing/shipping, and material handling equipment. Moving in a cost-effective way is important for businesses that are dealing with high volumes. In essence, WMS can improve inventory management, and lower labor costs. Current global events have capitulated the industry into a hyper-growth mode in this area. Two trends driving this are labor shortages and supply chain issues. Warehouse automation will offer a greater return on investment than human workers. This puts Zebra in a prime position to capitalize on these trends and meet customer demands, and scale output. In regards to labor shortages, the distribution centers need to look at different ways to fill orders. Being able to turn to warehouse automation can help a business scale more efficiently.

Looking a bit deeper into Industrial IoT (Internet of Things), this is critical to the success of warehouse automation. RFID is a good example because the tags placed on products can be tracked through every movement within the warehouse and more. The devices collect data and move it in real-time to create smarter decisions, predictive analysis, and more efficient operations for the business. The automated machines, which Zebra has just expanded through the acquisition of Fetch Robotics, can complete work without human input. Streamlining this sort of work optimizes the warehouse and drives costs down over time, once implemented, it is tough to leave.

Competitive Advantage

Zebra’s competitive advantage rests on the industry shift to the Android operating system, their economies of scale, and switching costs. These advantages should provide Zebra with a durable moat for years.

Operating Systems

Zebra was ahead of the competition predicting the Android operating system would become the dominant system. In 2011, the Microsoft OS was the preferred operating system for warehouse automation. Zebra was proven right in 2015 when Microsoft announced they would discontinue supporting their legacy system in five years.

In response, Zebra’s management announced a global initiative to help customers transition from the legacy Microsoft system to their Android system. VDC research estimates they sell over 58% of the new Android devices sold. The next closest competitor trails with only 12%.

Switching Costs & Economies of Scale

Zebra is embedded into their customers’ warehouse optimization system and it is a painful task to remove them. Customers would have to redesign their entire warehouse optimization system if they were to change products.

If a customer wanted to replace Zebra, it may have to find multiple vendors to accomplish the same tasks or face limits to its future capabilities. A Zebra replacement might be lacking in printing or RFID ability, for example, which would mean finding multiple vendors to accomplish what Zebra could do by itself. Zebra creates an even more integrated--and thus entrenched--system for its customers by layering software on top of its solutions. While Zebra's hardware forms the arms and legs of a customer's system--printing and scanning tags--the software, or brain, is what drives the bulk of the efficiency. - Morningstar

EVMs need to be replaced every 5-6 years. Given the challenges in changing products outlined above, companies won’t change unless they get a significant benefit or a significant discount. With 43 different offerings or 2.5 times more than their nearest competitor, Zebra’s product suite is more developed than their competitors. They describe the abundance of choices as “Right Size, Right Budget”. It is unlikely that a customer would receive significant benefits or a significant discount to entice them to switch. Zebra is also able to push through modest price increases with little pushback due to the aforementioned high switching costs.

Zebra’s closest competitor is Honeywell and they have multiple competitive advantages over Honeywell including customer base, research & development, and focus. Zebra’s existing customer base is massive and includes Amazon, UPS, FedEx, and even the NFL. High switching costs in the industry lock Zebra in with these lucrative customers. Honeywell is forced to target less lucrative customers that do not have established relationships due to these switching costs.

Zebra’s Customer Base

Source: Punch Card Investor

Zebra’s economies of scale allow them to have a higher research and development (R&D) budget than their competition. It is estimated Zebra outspends Honeywell in the AIT segment by over 100 million per year not including acquisitions. The higher R&D budget allows them to have a stronger, more complete product portfolio than their competitors while still being able to expand margins. Honeywell is a conglomerate and its focus is not solely on warehouse automation like Zebra. Focus is a big advantage for Zebra as well.

Management/Capital Allocation

Acquisitions

Zebra has made various acquisitions over the years. In this article, we will talk about the acquisitions made in 2021. To read about the acquisitions made in 2019 and 2020, click here.

Zebra’s acquisitions perfectly mold and expand their business model, strengthening their core competencies as well as being accretive relatively quickly.

The first acquisition was Adaptive Vision, this was a smaller one that they bought for around $18m in cash (net of cash acquired). The company supplies graphical machine vision software for the manufacturing industry (one of Zebra’s verticals). This will show up in the EVM segment. On their website, they have videos of reading barcodes, sorting, counting, and classifying defected objects, data matrices, and more. This fits very well with Zebra’s current product offerings.

The second acquisition is Fetch Robotics, Fetch is a provider of autonomous robots for businesses in the manufacturing, distribution, and fulfillment industries. This is a very fast-growing area in the market, and Zebra is expanding this in their EVM segment. This is a huge win for Zebra, (I) know some industry experts in this area of warehouse automation. Zebra paid $301m, $290m in cash, and the company’s existing minority ownership in Fetch of $11m.

Lastly, Antuit. This company was acquired for $145m in cash. They provide demand-sensing and pricing software for retail and consumer product companies. This suits Zebra very well, given they have customers like Target and Amazon.

Risks

Warehouse automation entails firing workers. This is good for companies but bad for workers. It is in many politicians' interests to slow or stop the automation of warehouses. While Zebra itself probably won’t face regulations, many of its customers likely will. This could be a significant headwind as customers are hesitant to further automate and adopt Zebra products.

Valuation

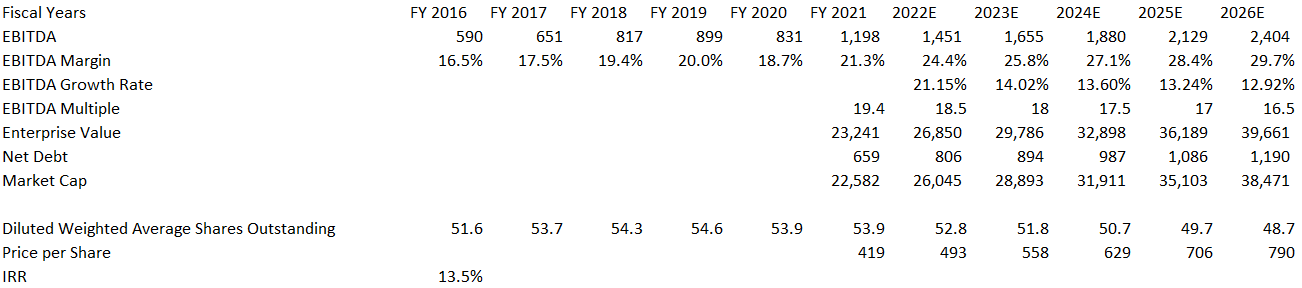

Zebra’s management team guided to 5-7% organic long-term revenue growth. Due to its history of under-promising and overperforming, it is reasonable to expect 6.5% of organic revenue growth. Zebra’s management also often makes tack on acquisitions and it is expected that would contribute 1.6% of revenue growth consistent with prior acquisitions. Gross margins should expand modestly as they transition to a SaaS offering and operating expenses should continue to decrease as they show economies of scale.

Source: Author, Historical Data from Koyfin

It is reasonable to assume that EBITDA will continue to outpace operating margins by 3.3%. Outside of 2022, it is expected that EBITDA will grow by low double digits. Multiple compression is expected, however, we do believe Zebra will continue to trade at a premium due to its strong competitive advantage. We also expect Zebra to continue its recent buyback and retire 2% of shares outstanding per year. If these assumptions are correct, Zebra will return a 13.5% IRR which implies an undervalued stock, however, not enough margin for safety to invest. On a downturn, I believe Zebra could be a good stock to invest in.

Source: Author, Historical Data from Koyfin

Disclosure: None of the Authors have a financial position in ZBRA, but could initiate one at any time. This is investment research, not investment advice, please do your own due diligence